Welcome reader, have you ever come across the term “structured settlement buyout” but don’t quite understand what it means? Well, you’re in luck! In this article, we’ll break down the basics of structured settlement buyouts in simple terms so you can grasp the concept easily. Whether you’re a recipient of a structured settlement or just curious about how these transactions work, we’ve got you covered. Let’s dive in and explore the world of structured settlement buyouts together!

What is a Structured Settlement Buyout?

A structured settlement buyout is a financial transaction in which an individual sells their future structured settlement payments to a third-party company in exchange for a lump sum of cash. Structured settlements are typically awarded to individuals who have suffered a personal injury or other type of financial loss and are designed to provide long-term financial security. However, there are times when the recipient may need immediate access to a larger sum of money, which is where a structured settlement buyout can be beneficial.

When a person decides to pursue a structured settlement buyout, they are essentially selling a portion or all of their future settlement payments to a company known as a “factoring company” or “settlement purchaser.” In return, the individual receives a lump sum payment that is typically discounted from the total value of the future payments. The amount of the lump sum payment will depend on various factors, including the total amount of remaining payments, the frequency of payments, and the current interest rates.

One of the main reasons why individuals choose to sell their structured settlement payments is to address immediate financial needs or opportunities. This could include paying off high-interest debts, covering medical expenses, purchasing a home or vehicle, starting a business, or investing in education. By selling their future payments, individuals have the flexibility to access a larger sum of money upfront rather than waiting for the periodic payments to be distributed over time.

It is important to note that the decision to sell structured settlement payments should not be taken lightly and requires careful consideration of the terms and conditions of the buyout agreement. While receiving a lump sum payment can provide immediate financial relief, individuals may end up receiving less money overall compared to continuing to receive the structured settlement payments as originally planned. Additionally, the fees and costs associated with a structured settlement buyout can vary among different companies, so it is essential to shop around and compare offers before making a final decision.

In conclusion, a structured settlement buyout offers individuals the opportunity to access a lump sum of cash by selling their future structured settlement payments to a third-party company. While this can be a helpful financial tool in certain situations, it is crucial to carefully weigh the pros and cons of a buyout before committing to the transaction. By seeking advice from financial advisors and exploring all available options, individuals can make informed decisions that align with their current and future financial goals.

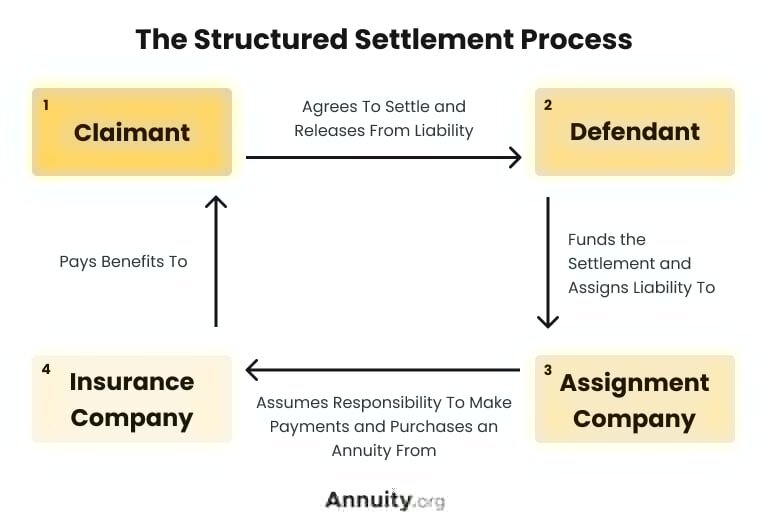

How Does a Structured Settlement Buyout Work?

When a person receives a structured settlement as a result of a personal injury lawsuit or other legal claim, they are typically given a series of regular payments over a set period of time. However, some people may find themselves in need of a lump sum of cash immediately rather than waiting for the payments to be disbursed over time. This is where a structured settlement buyout comes into play.

A structured settlement buyout involves selling some or all of the future payments from the settlement to a third-party buyer in exchange for a lump sum of cash. The buyer, also known as a settlement purchaser or factoring company, will pay the annuitant a discounted amount based on the present value of the future payments. The annuitant can then use this lump sum of cash for immediate expenses such as medical bills, debt repayment, or a large purchase.

The process of a structured settlement buyout typically involves the following steps:

1. Research and Comparison: The annuitant will research and compare different settlement purchasing companies to find the best offer for their structured settlement payments. It is important to work with a reputable and trustworthy company that offers competitive rates.

2. Application and Documentation: Once a settlement purchaser is selected, the annuitant will need to complete an application and provide documentation related to the structured settlement, including the settlement agreement, annuity contract, and payment schedule. The buyer will review this information to determine the value of the future payments.

3. Evaluation and Offer: The settlement purchaser will evaluate the structured settlement and make an offer to the annuitant. This offer will be based on factors such as the total amount of the future payments, the payment schedule, and the discount rate applied to calculate the lump sum payment.

4. Court Approval: In most cases, the sale of a structured settlement requires court approval. The annuitant’s best interest must be demonstrated to the court, and the judge will review the terms of the buyout agreement to ensure it is fair and in compliance with state laws.

5. Payment: Once the court approves the structured settlement buyout, the annuitant will receive the lump sum payment from the settlement purchaser. This payment can be used immediately for any expenses or investments the annuitant desires.

Overall, a structured settlement buyout can provide financial flexibility and relief to individuals who are in need of immediate cash. It is important to carefully consider all the factors involved in selling structured settlement payments and to work with a reputable company throughout the process.

Factors to Consider Before Selling Your Structured Settlement

Before making the decision to sell your structured settlement, there are several important factors that you should take into consideration. Selling your structured settlement can provide you with a lump sum of cash upfront, but it is important to weigh the pros and cons before moving forward.

1. Financial Needs: One of the most important factors to consider before selling your structured settlement is your current financial situation. Do you need immediate cash to cover medical expenses, pay off debt, or make a large purchase? If you are facing a financial emergency, selling your structured settlement may be the right decision for you. However, if you have stable finances and can meet your needs without selling your settlement, it may be better to hold onto it for the future.

2. Long-Term Impact: It is crucial to consider the long-term impact of selling your structured settlement. While receiving a lump sum of cash may seem enticing in the short term, you need to think about how it will affect your financial stability in the years to come. Will selling your settlement leave you in a worse financial position down the road? Will you be able to meet your future needs without the guaranteed payments from your settlement?

3. Consult with a Financial Advisor: Before making any decisions about selling your structured settlement, it is highly recommended to consult with a financial advisor. A professional advisor can help you evaluate your financial situation, assess the risks and benefits of selling your settlement, and create a plan that aligns with your long-term financial goals. They can provide you with valuable insights and guidance to ensure that you make an informed decision that is in your best interest.

4. Research Companies: If you do decide to sell your structured settlement, it is essential to do your research and choose a reputable company to work with. Look for companies with a good track record, positive reviews from previous clients, and transparent terms and conditions. Make sure to compare offers from multiple companies to ensure that you are getting the best deal possible.

5. Understand the Process: Selling your structured settlement can be a complex process, so it is important to fully understand how it works before moving forward. Make sure to ask questions, read the fine print, and seek clarification on any aspects of the sale that you are unsure about. By being informed and knowledgeable about the process, you can protect yourself from potential risks and make a sound decision that aligns with your financial goals.

Pros and Cons of Structured Settlement Buyouts

Structured settlement buyouts can provide a quick lump sum of cash to individuals who are receiving regular payments from a structured settlement. There are both pros and cons to consider before deciding whether to pursue a buyout.

Pros:

1. Immediate access to cash: One of the main advantages of a structured settlement buyout is that it provides immediate access to a significant amount of cash. This can be helpful for individuals who need money for emergencies, large purchases, or other financial needs.

2. Financial flexibility: By receiving a lump sum payment, individuals have the flexibility to use the money as they see fit. This can be especially beneficial for those who have specific financial goals or investments in mind.

3. Potential for higher returns: In some cases, investing the lump sum from a structured settlement buyout may lead to higher returns compared to receiving regular payments over time. This can be advantageous for individuals who are comfortable with taking on investment risk.

Cons:

1. Loss of future guaranteed income: One of the main drawbacks of a structured settlement buyout is the loss of future guaranteed income. Once a buyout is complete, individuals will no longer receive regular payments from the structured settlement.

2. Impact on financial planning: Structured settlements are often designed to provide a steady stream of income for an extended period of time. A buyout can disrupt long-term financial planning and may require careful consideration of how to manage the lump sum payment.

3. Tax implications: Depending on the amount of the lump sum payment, individuals may face tax implications that could reduce the overall benefit of the buyout. It’s important to consult with a financial advisor or tax professional to understand the potential tax consequences.

4. Pressure to spend or invest unwisely: When individuals receive a large sum of money all at once, there may be pressure to spend or invest the money unwisely. Without a structured plan for how to use the funds, there is a risk of running out of money or making poor financial decisions.

In conclusion, structured settlement buyouts can be a helpful financial tool for individuals who need immediate access to cash. However, it’s important to carefully weigh the pros and cons before making a decision. Consulting with a financial advisor or attorney can help individuals make an informed choice that aligns with their overall financial goals and needs.

Tips for Choosing a Reliable Buyer for Your Structured Settlement

When considering selling your structured settlement, it is crucial to choose a reliable buyer to ensure a smooth and transparent process. Here are some tips to help you find a trustworthy buyer:

1. Research the Company: Before deciding on a buyer, do some research on the company’s reputation. Look for reviews and ratings online, and check if they are accredited by organizations like the Better Business Bureau. A company with a good track record and positive feedback from previous clients is likely to be more reliable.

2. Compare Offers: Don’t settle for the first offer you receive. Shop around and compare offers from different buyers to ensure you are getting the best deal. Keep in mind that the highest offer may not always be the best option, so consider other factors like the buyer’s reputation and the terms of the agreement.

3. Transparency: A trustworthy buyer will be transparent about the entire process and provide you with all the information you need to make an informed decision. They should explain the terms of the agreement clearly and address any concerns or questions you may have. Avoid buyers who are vague or unwilling to provide details about the transaction.

4. Licensing and Regulation: Make sure the buyer is licensed and regulated by the appropriate authorities. This will ensure that they operate within the legal guidelines and adhere to industry standards. A licensed buyer is more likely to follow ethical practices and protect your rights as a seller.

5. Customer Service: One of the most important factors to consider when choosing a buyer is their customer service. A reliable buyer will have a team of knowledgeable and friendly representatives who are available to assist you throughout the process. They should be responsive to your inquiries and provide updates on the status of your transaction.

6. Flexibility: Look for a buyer who is flexible and willing to work with you to meet your specific needs. They should be open to negotiating terms and accommodating any requests you may have. Avoid buyers who have rigid policies and are unwilling to compromise.

By following these tips, you can choose a reliable buyer for your structured settlement and ensure a smooth and hassle-free transaction. Remember to take your time and carefully consider all your options before making a decision.